It's All Greek to Me

Quant Finance, Brainteasers, and Other Useful Things

Tuesday, January 3, 2012

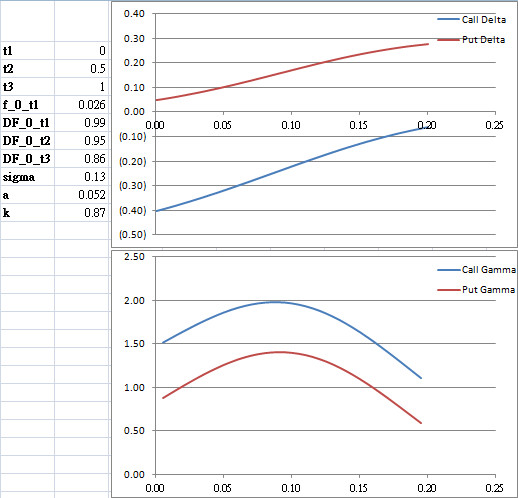

Short Rate Delta & Gamma (Hull-White One Factor)

Selection of European bond option greeks plots.

t2: option expiry

t3: underlying maturity

sigma: H-W volatility

a: H-W mean reversion

k: strike

x-axis: short rate

No comments:

Post a Comment

Newer Post

Older Post

Home

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment