Strategy 3): Hold VXX when the VIX term structure is in backwardation; hold XIV when it is in contango; and

Strategy 4): Hold VXX when recent realized vol is greater than VIX; hold XIV when recent realized vol is less than VIX

where contango and backwardation are defined by the levels of VIX (30 days variance swap rate) versus VXV (3 month variance swap rate).

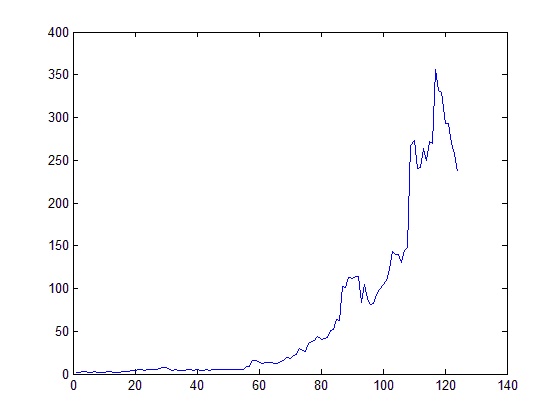

The problem is that historical data on both VXX and XIV are very limited (they go back only as far as late 2010). There is not much to do on Strategy 3), as VXV is a bottleneck. For Strategy 4)m though, I planned to retrospectively compute VXX and XIV prices pre-launch by using VIX future prices with their rebalancing rules. Fortunately the folk at The Intelligent Investor Blog has done exactly this, which saves me a lot of time and efforts. The following is the equity curve (start with $1; every time there is a signal, the liquidation amount is re-invested into the other ETN):