We have three securities (money market account, stock, call option on the stock with K = 100). Today their prices are [100, 100, 8]. Suppose one period from now the stock can end up being either in the high-volatility (in which case S = 120 or 80) or low-volatility (in which case S = 110 or 90) regime.The MMA would still be 100. Now consider an exotic option X. The payoff of X is (30, 0, 0, 15) corresponding to (high vol stock up, high vol stock down, low vol stock up, low vol stock down). You can imagine it as a derivative that becomes a call when volatility is high and a put otherwise. What is today's value of X?

Ans: $12

Note: This problem is solvable because the matrix that represents basis securities payoffs has a left inverse. When would this be not true? -> When some basis security is the linear combination of others.

Saturday, January 14, 2012

Thursday, January 12, 2012

Great link on swap spread

http://fermatslastspreadsheet.wordpress.com/2012/01/11/facts-intuition-and-rules-of-thumb-for-swap-spreads/

Not just introduces the concept but also discusses how to put it in credit/rates trading context.

Not just introduces the concept but also discusses how to put it in credit/rates trading context.

Tuesday, January 3, 2012

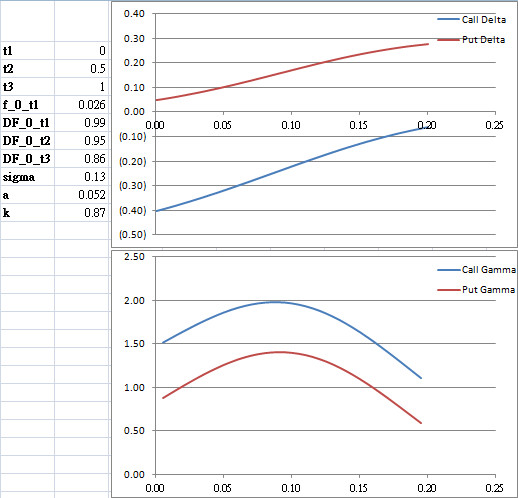

Short Rate Delta & Gamma (Hull-White One Factor)

Selection of European bond option greeks plots.

t2: option expiry

t3: underlying maturity

sigma: H-W volatility

a: H-W mean reversion

k: strike

x-axis: short rate

Pricing Callable Coupon Bond

Pricing a European callable zero-coupon bond is relatively straight forward. In fact, the callable zero-coupon bond can be decomposed into a non-callable zero-coupon bond and an European call option. Under many models (e.g. Hull-White), closed-form solution exists for European call option written on zero-coupon bond.

However, in reality, most callable corporate bonds bear coupons and the embedded options are American. In this case pricing would be much more complicated. First of all, since the embedded options are American, optimal exercise has to be considered. Secondly, the call on the principal plus the coupons cannot be seen as a basket of options because the option holder could only exercise the right to call everything, not an individual piece of cash flow.

There are at least 3 ways to tackle the pricing of callable coupon bonds:

However, in reality, most callable corporate bonds bear coupons and the embedded options are American. In this case pricing would be much more complicated. First of all, since the embedded options are American, optimal exercise has to be considered. Secondly, the call on the principal plus the coupons cannot be seen as a basket of options because the option holder could only exercise the right to call everything, not an individual piece of cash flow.

There are at least 3 ways to tackle the pricing of callable coupon bonds:

- Structural model - much like the structural credit models, we can postulate a model that describes how exercise strategy and hence option price are affected by the goal to minimize firm liabilities, by assuming a stochastic firm value process. Like other structural models, the drawback is that complete firm information is required.

- Reduced form model (American option) - this is similar to the pricing of callable zero-coupon bonds, namely by explicitly considering the embedded call. The drawbacks are that a) the bond can never exceed par (the same problem arises in MBS reduced form pricing), and b) numerical method is necessary.

- Reduced form model ("call intensity") - Jarrow et al proposes a method that treats the call feature as a hazard besides credit default risk. The approach is very similar to the reduced form model of Duffie and Singleton 1999. If the call intensity process is affine, closed-form solution exists.

Subscribe to:

Posts (Atom)